The Risk Is Not the Client. The Risk Is the Process.

There is a version of AML compliance that looks correct on paper and fails completely in practice. It has documented policies, a designated compliance officer, client verification procedures, and a SAR filing process. It satisfies the form of compliance while systematically undermining its substance. And the mechanism through which it fails is one of the most pervasive and least acknowledged problems in real estate AML: the quiet, recurring, commercially rational decision to apply the rules differently depending on the size of the deal.

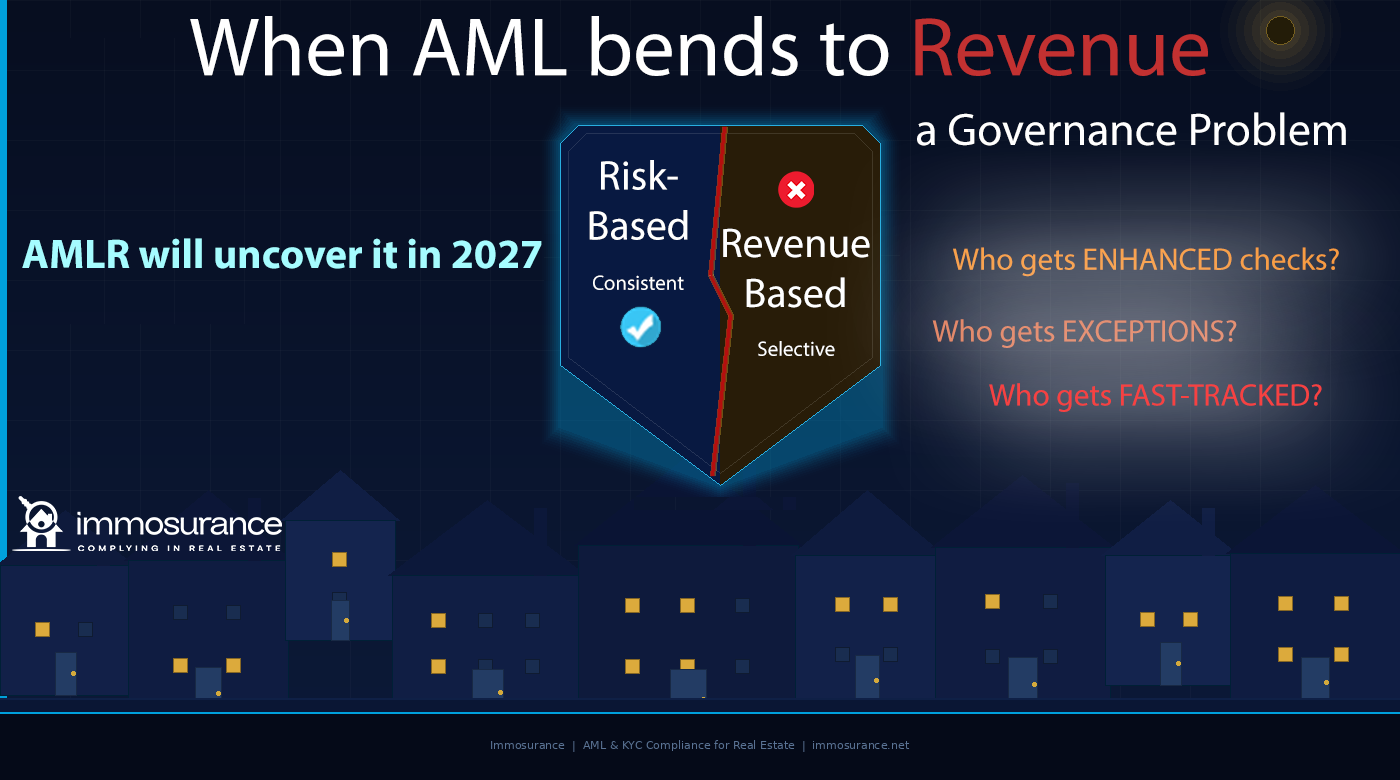

The source article from which this one grows makes a precise and uncomfortable observation: when revenue pressure is present, AML becomes flexible. The decision about which clients receive enhanced checks, which get exceptions, and which get fast-tracked is not made on the basis of risk — it is made on the basis of profit. And that is not a risk-based approach. It is a revenue-based approach dressed in compliance language. Regulators, supervisors, and increasingly AMLA — the new EU Anti-Money Laundering Authority — know exactly what it looks like, and they test for it specifically.

Under Regulation (EU) 2024/1624, the EU's Anti-Money Laundering Regulation applicable from July 2027 across all 27 member states, the standard is not just that AML obligations exist. It is that they are applied consistently. The consistency requirement is not incidental — it is the operational heart of the risk-based approach. A compliance programme that is selectively rigorous is not a risk-based programme. It is a governance failure. And from July 2027, that failure will be directly detectable, directly attributable, and directly enforceable.

This article examines how commercial pressure corrupts AML compliance in real estate, why the AMLR makes inconsistency specifically dangerous, what the real diagnostic questions are for any business that wants to know whether its AML is genuinely risk-based or covertly revenue-based, and how Immosurance — Europe's only purpose-built AML compliance platform for real estate — provides the structural answer to a problem that policy documents alone cannot solve.

The Two Faces of Commercial Pressure in Real Estate AML

Commercial pressure corrupts AML compliance in real estate through two distinct mechanisms, and both are more common and more consequential than most businesses acknowledge.

"Policy Says No" When the Real Reason Is Commercial Discomfort

The first mechanism is the use of compliance language to justify a commercial decision. A client whose transaction presents genuine AML risk is declined or subjected to enhanced scrutiny — but the stated reason is "our policy requires us to..." rather than "this transaction presents specific risk factors that we cannot manage." The policy becomes a rhetorical shield for a decision that is, at bottom, commercially motivated.

This might seem like a minor semantic issue. It is not. The distinction matters for several reasons.

First, it means the compliance decision is not documented with the risk reasoning that AML law requires. The AMLR mandates documented, evidence-based risk assessments. "Policy says no" is not a risk assessment. It is a policy invocation. Where a SAR is required — because the declined transaction presented reasonable grounds for suspicion — the absence of documented risk reasoning means the SAR obligation is not met.

Second, it means the decision-making process is not transparent or auditable in the way the AMLR demands. A regulator examining a compliance file wants to see: what risk was identified, what evidence supported that identification, what investigation was conducted, and what conclusion was reached. A file that shows only "declined per policy" demonstrates nothing except that a policy existed.

Third — and most relevant to the commercial dynamics of real estate — it means that "policy says no" can be selectively invoked. The same policy provision that justifies declining a modest transaction from an unfamiliar buyer can, with slightly different emphasis, be read as permitting a similar transaction from a high-value client. The policy has not changed. The commercial interest has. And the compliance outcome has changed with it.

"Policy Allows It" When the Real Issue Is Revenue Pressure

The second, and more serious, mechanism is the opposite: using policy flexibility as permission to proceed with a transaction that should be declined or escalated, because the commercial value of the transaction creates pressure to find a path through.

Every AML framework contains zones of discretion. The risk-based approach requires professionals to assess risk and apply proportionate controls — which means that some decisions require judgment rather than mechanical rule application. That discretion is a feature of the framework, not a flaw: it enables proportionate responses to genuinely varied risk profiles.

But discretion is also a vulnerability when revenue pressure is present. The agent who decides that a high-value transaction from a client with a complex corporate structure "can proceed" because "the policy allows discretion" has made a compliance decision — but the deciding factor was not the risk assessment. It was the commission. The policy language provides cover for what is, in substance, a revenue-driven outcome.

This is what the source article means by "when the real issue is revenue pressure, AML becomes flexible depending on profit." The flexibility is real. The policy framework genuinely contains it. But the application of that flexibility is corrupted when its driver is profit rather than risk.

In real estate, where transaction values are high, commissions are significant, and client relationships are personal and long-standing, this corruption is structurally predictable. It does not require dishonesty or conscious bad faith. It requires only the normal human tendency to find permission for what one is already commercially motivated to do.

The Three Questions That Reveal Whether Your AML Is Risk-Based or Revenue-Based

The source article identifies three diagnostic questions that supervisors use — and that every real estate compliance officer should ask about their own business — to determine whether the risk-based approach is genuinely operating or whether it has been quietly replaced by a revenue-based equivalent.

Who Gets Enhanced Checks?

In a genuinely risk-based programme, Enhanced Due Diligence is applied to customers and transactions that present elevated risk indicators: PEP connections, high-risk country involvement, complex ownership structures, non-face-to-face relationships, unusual transaction structures. The risk profile determines the due diligence level, not the commercial value of the deal.

In a revenue-based programme, EDD tends to be applied to smaller transactions and less commercially significant clients — the ones where the commercial cost of the compliance friction is low — while high-value clients receive lighter treatment on the grounds that "we know them well," "they're a long-standing client," or "the deal is time-sensitive."

The diagnostic test is simple: look at the EDD records for the last twelve months. Are they concentrated in smaller-value transactions? Are the high-value clients consistently classified as standard risk? Do the risk classifications correlate with revenue rather than with risk factors? If so, the programme is revenue-based.

Who Gets Exceptions?

Every AML programme has exceptions — cases where the normal process was not followed, was abbreviated, or was substituted with alternative documentation. Exceptions are legitimate in principle: genuine commercial necessity, unforeseen circumstances, or client-specific considerations can justify departures from standard procedures, provided they are documented and approved.

But exceptions that cluster around certain client profiles reveal a pattern. If exceptions are granted disproportionately to high-value clients, to clients with whom principals have personal relationships, or to transactions where the commercial pressure to close is highest, the exception is not a risk-based judgment. It is a commercially motivated departure from the compliance standard that the policy ostensibly requires.

Under the AMLR, exceptions must be documented, justified with reference to specific risk factors, and approved at the appropriate level of governance. An undocumented exception — or one documented only with "approved by [partner]" without a risk rationale — is a compliance failure regardless of the commercial logic that drove it.

Who Gets Fast-Tracked?

Time pressure is one of the most reliable vectors through which commercial considerations corrupt compliance. A transaction that is moving quickly, where the buyer is motivated, where the seller is pressing for completion, and where the agent's commission depends on exchange — creates pressure to accelerate the compliance process in ways that compromise its quality.

Fast-tracking a CDD process means something is being skipped or assumed rather than verified. It means verification is happening concurrently with transaction progression rather than before it, in breach of the AMLR's sequencing requirement. It means the risk assessment is being produced to justify a predetermined decision rather than to inform one.

The pattern of which transactions get fast-tracked, and whether that pattern correlates with transaction value, reveals whether the compliance process is genuinely setting the pace of business or whether business is dictating the pace of compliance. Under the AMLR, the answer is unambiguous: CDD must be completed before the business relationship is established. There is no exception for commercial urgency.

Why the AMLR Makes Inconsistency Specifically Dangerous

Previous EU AML frameworks created the legal obligation of consistency but varied significantly in the rigour with which they enforced it. The AMLR changes this in ways that make revenue-based AML a much more acute legal risk than it has previously been.

Direct applicability eliminates national variation. Under the Directive framework, the requirement of consistency was interpreted and enforced differently in different member states. Some national supervisors accepted a relatively low standard of documented evidence for risk classifications; others required detailed justification. The AMLR applies identically in every member state, and the consistency standard it imposes is the highest that has ever been directly applicable across the EU.

AMLA tests for pattern-level inconsistency. AMLA's supervisory mandate — explicitly stated in Regulation (EU) 2024/1620 — includes assessing not just whether individual compliance decisions are correct but whether they are consistently applied across the business. This is supervisory pattern analysis: examining whether EDD triggers are applied with the same rigour to high-value clients as to lower-value ones, whether exceptions are distributed randomly or concentrated among commercially significant relationships, and whether the pace of compliance processes varies systematically with transaction value.

A business that has good compliance documentation for its smaller deals and loose documentation for its larger ones has, in effect, produced documentary evidence of a two-tier compliance system. That evidence will not help it in a supervisory inspection. It will be the primary exhibit.

Governance failures are personal. Under the 6th AMLD and the AMLR's framework, senior management responsibility for AML compliance is explicitly established. Where a compliance programme fails not through ignorance but through the systematic accommodation of commercial pressure — where management has, in effect, decided that large deals are treated differently — the individuals who made those decisions carry personal exposure. This is not merely a corporate liability. It is a personal one, potentially including criminal liability for the most serious failures.

The letting market is newly exposed. The AMLR's extension of obliged entity status to letting agents at the €10,000/month threshold introduces a category of professionals who have not previously operated within a formal AML framework. The commercial pressure dynamics in the lettings market — where competition for high-value landlord mandates is intense, where personal relationships drive business, and where the temptation to find compliance paths through for commercially important clients is structurally similar to the sales market — are exactly the dynamics that create revenue-based AML risk. Starting a compliance programme that is already corrupted by commercial pressure is worse than having no programme at all: it creates a documented record of selective application.

The Governance Problem: Why Policy Alone Cannot Solve It

The source article makes a statement that deserves careful attention: if your AML decisions change with pressure, you have a governance problem. Not a policy problem. Not a training problem. A governance problem.

The distinction is important because it determines the solution. A policy problem is solved by improving the policy. A training problem is solved by improving training. A governance problem — a problem with the structure of decision-making, accountability, and the mechanisms through which pressure is translated into outcomes — is solved only by changing the structural conditions that produce the problem.

In real estate, the governance problem created by commercial pressure has three dimensions:

Decision-making at the wrong level. When compliance decisions are made by the agent handling the transaction, the person making the decision has both the most commercial interest in the outcome and the least compliance expertise. The AMLR's compliance officer requirement exists precisely to address this: material compliance decisions must be escalated to the compliance officer, who has designated responsibility for the decision and who is structurally separated from the commercial outcome. A business in which agents make their own compliance decisions — however well-trained they are — does not have the governance structure the AMLR requires.

The absence of a documented risk rationale. Governance problems become visible when decisions cannot be justified with documented risk reasoning. A business that processes transactions by collecting documents and making informal judgements produces no evidence of risk-based decision-making, because the decision-making process is entirely internal. A regulator examining such a business cannot tell whether its decisions were risk-based or revenue-based, because there is no documentation of either. The documentation obligation is not merely a record-keeping requirement — it is the mechanism through which governance accountability is established and tested.

No structural check on exception-granting. In businesses where exceptions require only informal senior approval, the structural check on exception-granting is as strong as the senior person's willingness to apply it consistently under commercial pressure — which is to say, not very strong. The AMLR's governance requirements create the expectation of formal, documented exception processes with defined approval authorities and documented rationales. An exception that exists only in an email chain between a principal and an agent is not a governed exception. It is a discretionary departure with no accountability.

What Genuinely Risk-Based AML Looks Like in Real Estate

The alternative to revenue-based AML is not merely policy-compliant AML. It is structurally enforced risk-based AML — where the risk classification is produced by a documented process, the due diligence level is determined by the classification, the sequencing is enforced before the transaction proceeds, exceptions require documented risk-based justification, and the compliance officer makes material escalation decisions without commercial interference.

The practical markers of a genuinely risk-based programme in real estate are:

EDD is applied to large high-value transactions more often than to small ones — because large, high-value transactions from wealthy buyers, international buyers, and corporate buyers present more risk factors, not fewer. A compliance programme in which EDD correlates inversely with transaction value has the relationship backwards.

Exceptions require documented risk rationale — not just approval. The document shows why the normal process was modified, what specific risk factors were assessed, and why the modified process was judged adequate in the circumstances.

The compliance officer reviews and approves material exceptions — not the commercial principal who has a financial interest in the transaction proceeding.

The compliance timeline is determined by the risk assessment — not by the commercial urgency of the deal. Fast-tracking happens by accelerating the compliance process through better tools, not by compressing or skipping steps.

Risk classifications are reviewed and challenged — by the compliance officer, on a sample basis, to test whether classifications reflect genuine risk analysis or commercial rationalisation.

New clients receive the same process as established clients — the fact that a professional "knows" a client is not a substitute for documented verification. Personal knowledge is not verifiable evidence. The AMLR's standard requires independent verification regardless of the personal relationship.

How Immosurance Removes the Structural Conditions That Enable Revenue-Based AML

The governance problem created by commercial pressure cannot be solved by policy alone because policy does not change the structural conditions that produce commercial pressure. It can only be solved by an infrastructure that makes consistent compliance the path of least resistance — where the steps that are required are enforced by the system, where exceptions require documented justification that is visible to the compliance officer, and where the risk classification is produced by an objective process rather than a commercial judgment.

This is precisely what Immosurance is designed to do.

Structural enforcement of the risk-based approach. The Immosurance onboarding workflow enforces the AMLR's sequencing requirement structurally: CDD must be completed before the dossier can proceed. There is no fast-track option that bypasses required steps. The risk classification is generated by the Real Estate Risk Module from the verified data — not entered manually by the agent handling the transaction. A high-value transaction with a complex corporate structure receives the same risk assessment methodology as a straightforward domestic purchase. The agent cannot reclassify a customer as standard risk because the deal is commercially important.

Compliance officer oversight by design. The platform's role-based architecture routes material compliance decisions — EDD escalations, exception approvals, SAR consideration decisions — to the compliance officer role, not to the agent role. The compliance officer sees every escalation, every exception request, and every SAR consideration. The commercial separation that the AMLR's governance structure requires is built into the system, not dependent on the self-discipline of individuals under commercial pressure.

Documented, auditable decision trails. Every compliance decision — the risk classification rationale, the EDD trigger assessment, the exception approval with its documented justification, the SAR consideration outcome — is recorded in the client dossier with a timestamp and the identity of the decision-maker. A regulator or AMLA supervisor examining this record sees not just what decision was made but the complete evidence base for it. The pattern of decisions — which clients received EDD, which received exceptions, which were fast-tracked — is visible in aggregate across the dossier history. If that pattern is consistent with genuine risk-based application, the record demonstrates it. If it is consistent with revenue-based application, the record exposes it.

Exception management that creates accountability. Where the normal process must be modified, Immosurance's exception workflow requires a documented risk rationale, escalation to the compliance officer, and a recorded approval decision. An undocumented exception — the informal "we'll sort the documentation later" that characterises commercially pressured compliance — cannot occur within the platform's architecture, because the dossier remains incomplete until the required documentation exists.

Consistency verification. The compliance officer's dashboard provides an aggregate view of risk classifications, EDD applications, and exception grants across the business's entire client portfolio. This is the tool that makes the three diagnostic questions — who gets enhanced checks, who gets exceptions, who gets fast-tracked — answerable with data rather than impression. If the pattern is consistent, the dashboard confirms it. If it is not, the dashboard makes the inconsistency visible to the compliance officer — before a regulator does.

The Commercial Case for Consistent AML

The source article frames the problem correctly: revenue pressure creates flexible AML, and flexible AML is a governance problem. But it is worth adding a dimension that the compliance framing alone does not fully capture: consistent AML is also a commercial advantage.

Real estate professionals who operate in the international, institutional, and high-value market segments — the very segments where commercial pressure to accommodate clients is most intense — are also the segments where clients increasingly scrutinise the compliance standards of the professionals they work with. An institutional investor, a family office, a REIT acquiring assets across multiple EU markets: these are clients who cannot afford association with a professional whose compliance programme is selective. The agent who can demonstrate a structured, documented, consistently applied compliance programme — supported by institutional-grade technology — wins mandates that the agent with informal, discretionary processes cannot access.

Consistent AML is also reputational insurance. A professional who applies EDD rigorously to a large transaction from a complex corporate structure, documents the investigation thoroughly, and declines to proceed when the risk cannot be managed, has a complete compliance record to present in any subsequent regulatory or legal inquiry. The professional who fast-tracked the same transaction because it was commercially attractive has the opposite: a record that demonstrates the compliance failure precisely when the transaction later attracts attention.

Conclusion: The Risk Is Not the Client. The Risk Is the Process.

The source article ends with a statement that should be the working principle of every real estate compliance officer in Europe: if your AML decisions change with pressure, you have a governance problem.

The AMLR's July 2027 application date makes that governance problem legally consequential. AMLA's supervisory mandate makes it detectable. And the personal liability provisions of the 6th AMLD make it personal.

The solution is not stricter policy language. Policies are only as strong as the governance structures that enforce them. The solution is structural: compliance processes that enforce consistent risk-based treatment regardless of commercial pressure; decision-making authority that is separated from commercial interest; documentation standards that record not just what was decided but why; and oversight mechanisms that make consistency measurable and visible.

Immosurance provides that structure. It does not change the commercial pressures that real estate professionals face — those are inherent to the sector and will not disappear. What it does is remove the discretion through which those pressures corrupt compliance, and replace it with a system where the risk-based approach is enforced by architecture rather than willpower.

Every real estate business in Europe will face the AMLR standard from July 2027. The ones that face it with a governance structure that produces genuinely consistent compliance will be ready. The ones that arrive with revenue-based AML in compliance clothing will face exactly the pattern-level scrutiny that AMLA is designed to apply. Preparing takes time, resources and dedication: the time to start is now.

The choice of which category to be in is still available. Immosurance is how to make it.