What Is a SAR

What Is a SAR — and Why Every Real Estate Professional in Europe Must Understand It

There is a line that separates a real estate professional who has done their legal duty from one who has not. It is drawn not at the point of identity verification, not at the point of source of funds collection, and not at the point of risk assessment — though all of those obligations matter. The line is drawn at the moment when a professional who has identified suspicious activity decides what to do next.

Filing a Suspicious Activity Report — a SAR — is what doing the right thing looks like in practice. It is the mechanism through which real estate professionals discharge the most consequential obligation in the AML/CFT framework: the obligation not merely to detect potential financial crime, but to report it to the national Financial Intelligence Unit (FIU) so that law enforcement and regulators can act on it.

Under Regulation (EU) 2024/1624 — the EU's Anti-Money Laundering Regulation (AMLR), directly applicable across all 27 member states from July 2027 — the SAR obligation is mandatory, enforceable, and attended by both legal protections for those who report in good faith and serious legal consequences for those who fail to report at all. For real estate professionals who have historically treated suspicious activity reporting as someone else's concern, the AMLR makes clear: it is yours.

Learn what a SAR is, what triggers it in the specific context of real estate transactions, what the AMLR requires of professionals before and after filing, what legal protections apply, and how Immosurance — Europe's only purpose-built AML compliance platform for real estate — provides the infrastructure to detect, investigate, document, and file correctly and consistently.

What Is a SAR?

A Suspicious Activity Report is a formal notification filed by an obliged entity — including real estate professionals — with the national Financial Intelligence Unit when the filer has reasonable grounds to suspect that funds involved in a transaction or business relationship are the proceeds of criminal activity, or are connected to money laundering or terrorist financing.

The key phrase is reasonable grounds to suspect. This is a deliberately low threshold. It does not require proof. It does not require certainty. It does not require the professional to have conducted a full investigation and reached a definitive conclusion. It requires that, based on observable facts, documented behaviour, and the professional's knowledge of the customer and transaction, a reasonable person in that position would consider it more likely than not that something is wrong.

This standard has two important practical implications. First, it means the threshold for filing is lower than many professionals assume: you do not need to be sure before you report. Second, it means the threshold is not zero: vague unease, general discomfort, or a sense that something feels "off" without any documented factual basis does not satisfy it. The reasonable suspicion standard sits between instinct and certainty — and it is where documented AML/KYC processes create the evidence base that allows professionals to identify and articulate it correctly.

In some EU member states, the equivalent report is called a Suspicious Transaction Report (STR). The terminology varies nationally, but the underlying obligation under the AMLR is the same: where there are reasonable grounds for suspicion, the professional must report.

Why Real Estate Is a Priority Sector for SAR Obligations

Financial Intelligence Units across Europe receive SARs from a wide range of obliged entities — banks, payment institutions, accountants, lawyers, and others. Real estate professionals have historically been among the most underperforming reporters: SAR volumes from the sector have been consistently low relative to the documented prevalence of money laundering through property transactions.

The gap between the scale of the risk and the volume of reporting reflects the compliance infrastructure deficit described throughout this series. Professionals who have no systematic process for identifying red flags cannot identify the reasonable suspicion that triggers a SAR obligation. Professionals who have no documented investigation process cannot articulate the factual basis for their suspicion. And professionals who have no SAR-filing infrastructure — no designated compliance officer, no internal escalation pathway, no secure channel to the FIU — cannot file even when they know they should.

The AMLR is designed specifically to close this gap. By mandating not just the reporting obligation but the underlying compliance infrastructure — risk assessments, CDD processes, ongoing monitoring, compliance officer designation, staff training — it creates the conditions under which SAR obligations can actually be met. The obligation to report is inseparable from the obligation to detect. And the obligation to detect is inseparable from the obligation to build the processes that make detection systematic rather than accidental.

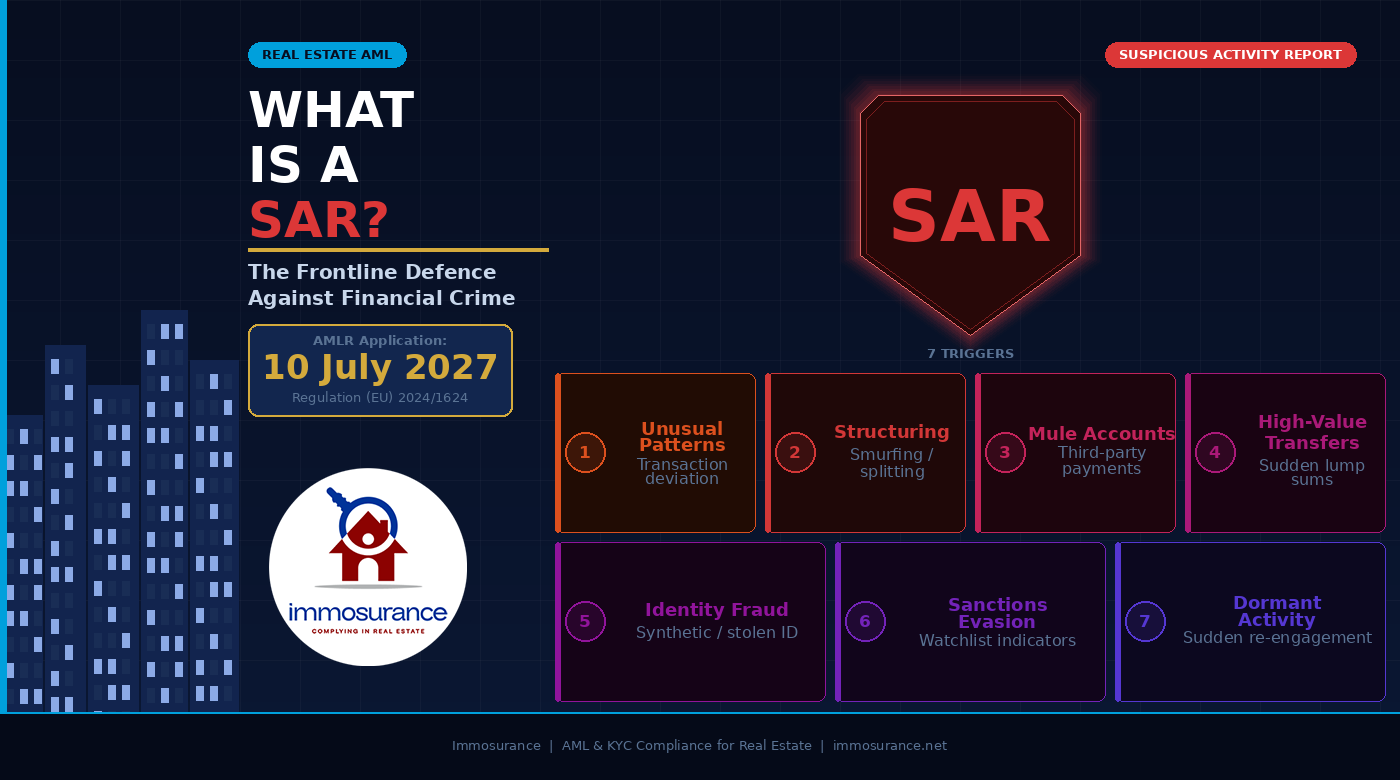

What Triggers a SAR in Real Estate: The Seven Key Categories

Each of the SAR triggers described in the source article manifests in real estate in ways that are distinct from their banking or financial services equivalents. Understanding those manifestations is what gives real estate professionals the practical ability to apply the reasonable suspicion standard correctly.

1. Unusual Transaction Patterns

In real estate, the "usual" transaction pattern for a given customer is established at onboarding: the declared purpose of the relationship, the expected transaction type, the anticipated value range, the declared source of funds, and the stated investment objectives. An unusual pattern is anything that departs materially from that established profile without a plausible explanation.

Examples include: a residential buyer who suddenly introduces a complex corporate ownership structure for what was declared as a personal purchase; an investor whose transaction frequency accelerates dramatically without any declared change in investment strategy; a landlord whose declared rental income bears no relationship to the portfolio size; or a buyer who, midway through a transaction, changes the purchasing entity without explanation.

Under the AMLR's ongoing monitoring obligation (Article 26), these deviations must be identified systematically, investigated promptly, and documented whether or not they ultimately result in a SAR filing.

2. Structuring and Smurfing

Structuring — the deliberate division of a large sum into smaller amounts to avoid detection thresholds — is one of the most directly prosecutable money laundering offences under EU law and one of the clearest SAR triggers in real estate.

In a property context, structuring appears as multiple smaller payments from different accounts or individuals that together constitute a large deposit; payments timed specifically to remain below the EU's harmonised €10,000 cash threshold; or the use of multiple agents, notaries, or jurisdictions to divide a single economic transaction across multiple apparently smaller ones. The common element is intentionality: the structure of the payment arrangement makes commercial sense only if the purpose is to avoid detection.

Where structuring is identified, the reasonable suspicion threshold is likely met immediately. The professional should not seek additional confirmation from the customer — that risks tipping off — but should proceed directly to internal escalation and SAR consideration.

3. Mule Account Activity

A mule account is an account used — wittingly or unwittingly — to receive and transfer funds on behalf of a criminal. In real estate, mule account activity typically manifests as payments arriving from accounts with no apparent connection to the named buyer: a different individual, a company with no relationship to the transaction, or accounts in jurisdictions entirely unrelated to the buyer's declared profile.

This is one of the most consistently cited red flags in FATF and Europol guidance on real estate money laundering, and it is one of the most frequently encountered. A buyer whose deposit arrives from his cousin's company in a third country, or whose purchase funds come from an account in a jurisdiction where the buyer has no declared business interests, presents a clear factual basis for investigation and, depending on the explanation obtained, for SAR filing.

The AMLR's source of funds obligation directly addresses this trigger: professionals must not merely confirm that funds exist but must trace them to their legitimate origin. Where the origin is a mule account — even an unknowing one — the funds cannot be traced to a legitimate source, and the reasonable suspicion threshold is met.

4. Sudden High-Value Transfers

A sudden high-value transfer — funds arriving in a customer's account or in the transaction account in a lump sum without a documented prior history of such accumulation — is a placement indicator. It suggests that criminal proceeds are being introduced into the financial system at the point of the real estate transaction.

In real estate, this appears as a buyer who suddenly has the full purchase price available in cash or as a recent large bank transfer, with no documented history of the gradual accumulation that legitimate savings or investment proceeds would show. The contrast between the declared economic profile and the sudden availability of large funds is the trigger.

Under EDD, the professional must obtain Source of Wealth documentation that explains not only where the specific funds came from but how the customer accumulated their total wealth. Where that documentation is unavailable or implausible, the reasonable suspicion threshold is met.

5. Identity Theft and Synthetic Identities

Identity fraud in real estate takes several forms: the use of stolen identity documentation to impersonate a legitimate buyer or seller; the creation of synthetic identities — combinations of real and fabricated data — that pass basic verification but are not connected to any real natural person; and the impersonation of a legitimate property owner in order to sell a property without the owner's knowledge.

The AMLR's biometric and documentary verification requirements — which Immosurance delivers through IDVerse — are specifically designed to detect identity fraud by matching a live facial image against government-issued documentation. Where verification fails or produces inconsistencies, the professional must investigate. Where verification passes but other factors create doubt about the customer's true identity, the professional must document that doubt and assess whether the reasonable suspicion threshold is met.

Identity fraud in real estate is not purely an AML concern — it is also a direct financial fraud risk that affects victims in the most concrete way imaginable. But the AML compliance process is the primary mechanism through which it is detected, and the SAR is the mechanism through which it is reported.

6. Sanctions Evasion Indicators

Sanctions evasion — the use of intermediaries, front companies, or complex corporate structures to conduct transactions on behalf of sanctioned persons or entities — is a criminal offence that real estate professionals can inadvertently facilitate if their screening processes are inadequate or their understanding of the indicators is limited.

In real estate, sanctions evasion indicators include: corporate purchasing entities with opaque beneficial ownership that cannot be resolved to a verified natural person; transactions involving jurisdictions subject to targeted sanctions regimes; unexplained third-party payments from sources with connections to sanctioned states or individuals; and sudden urgency to complete a transaction without adequate time for due diligence — a pressure tactic used by those who know that thorough screening would reveal a problem.

Under the AMLR, sanctions screening is a continuous obligation, not a one-time check. Where LexisNexis screening (integrated in Immosurance) generates a match or a near-match against any applicable sanctions list, the professional must immediately freeze the transaction, investigate the match, and — where a genuine match is confirmed — report to the competent national authority in accordance with the applicable sanctions reporting requirements. The SAR mechanism is separate from sanctions reporting but may be required simultaneously.

7. Dormant Accounts and Relationships Suddenly Becoming Active

In real estate, the equivalent of a dormant account is a client relationship that has been inactive for an extended period and suddenly re-engages with an unusual level of urgency or with a transaction profile materially different from the prior history of the relationship.

A landlord who has managed the same portfolio quietly for five years and suddenly seeks to sell every property within a short period; a buyer who purchased a single residential property a decade ago and now approaches with a complex multi-property investment acquisition using offshore funding; a developer who was inactive for three years and returns with a project financed through an opaque foreign entity — these patterns of sudden re-engagement combined with elevated risk indicators can constitute reasonable grounds for suspicion.

The AMLR's periodic KYC refresh obligation, triggered at risk-appropriate intervals, is the mechanism through which dormant relationships are reassessed when they become active again. Where the reassessment reveals material changes in the risk profile that cannot be satisfactorily explained, SAR filing must be considered.

The SAR Filing Process: What the AMLR Requires

The AMLR and the companion 6th AMLD establish a clear procedural framework for SAR filing that real estate professionals must understand and implement.

The Internal Escalation Requirement

Before a SAR is filed with the national FIU, it must pass through the professional's internal compliance process. This means the concern must be identified — whether through ongoing monitoring, a risk alert, a compliance officer review, or a staff member's observation — and escalated to the designated AML compliance officer. The compliance officer must then conduct or oversee an investigation that produces a documented assessment of the facts, the indicators of suspicion, and the conclusion reached.

The AMLR requires that the compliance officer role be designated and documented. A real estate business in which anyone other than the designated compliance officer makes SAR-filing decisions — or in which SAR decisions are made ad hoc without a documented assessment — does not meet the structural requirement of the regulation.

The Documentation Requirement

The investigation that precedes a SAR decision must be documented in sufficient detail to demonstrate that:

· The facts giving rise to the concern were accurately identified

· The investigation was conducted systematically and in good faith

· The customer or transaction profile was considered holistically, not in isolation

· The conclusion reached — to file or not to file — was based on the documented facts and the reasonable suspicion standard

This documentation is what distinguishes a compliant SAR filing from an unconsidered one, and a compliant decision not to file from an unlawful failure to report. Both filing and not filing must be defensible, and the documentary record is what makes them so.

The Tipping-Off Prohibition

One of the most important — and most frequently misunderstood — provisions of the AML/CFT framework is the tipping-off prohibition. Under EU law, and specifically under the 6th AMLD, it is a criminal offence to inform a customer, or any person associated with them, that a SAR has been or will be filed, or that they are the subject of an AML investigation.

For real estate professionals, who often have personal relationships with clients built over years of professional engagement, this prohibition creates a specific and serious challenge. The natural instinct — to be transparent, to give the client a chance to explain before taking action — is legally prohibited once reasonable suspicion has been formed. The investigation must be conducted internally. The SAR must be filed without warning. And ongoing communication with the client must not reveal, even by implication, that anything is unusual about the compliance treatment of their matter.

This does not mean the professional cannot continue to engage with the client normally in commercial matters while the SAR process is underway. It means they cannot disclose the compliance concerns or the reporting activity. The line between normal commercial engagement and prohibited disclosure requires careful management, and in cases of doubt, legal advice should be sought.

The Good-Faith Protection

The 6th AMLD introduces an explicit protection for professionals who file SARs in good faith: immunity from civil and criminal liability arising from the report, provided it was made in good faith and in accordance with the applicable legal requirements. This protection directly addresses one of the most commonly cited reasons for SAR non-filing in the real estate sector — the fear of legal consequences if the suspicion ultimately proves unfounded.

The protection is real and significant. A professional who files a SAR based on documented reasonable suspicion, following a conducted investigation, through the appropriate FIU channel, cannot be sued by the customer for defamation or breach of confidentiality, and cannot face criminal prosecution for breach of privacy. The documentation of the investigation process is what establishes the good faith that the protection requires.

The Timing Requirement

SARs must be filed promptly. The AMLR and national implementing legislation establish timelines for reporting that vary by circumstance — some jurisdictions require reporting within 24 hours of forming a suspicion in urgent cases, others within a specified period. Real estate professionals must understand the applicable national timeline and ensure that internal processes do not create delays between forming a suspicion and filing the report.

Where filing a SAR before a transaction completes would alert the customer to the investigation (because, for example, a delay in completing would be inexplicable), the professional may need to seek guidance from the national FIU on how to proceed. In some cases, the FIU can issue a consent or direction that allows the transaction to proceed for intelligence purposes. This is not an excuse to delay filing — it is a specific procedure for cases where completing the transaction before disclosing the concern is operationally necessary for law enforcement purposes.

Five Principles Every Real Estate Compliance Officer Must Apply

The source article's key takeaways for AML professionals translate directly into operational guidance for real estate compliance officers under the AMLR framework.

Focus on facts, behaviour, and evidence — not assumptions. The reasonable suspicion standard requires an objective, evidence-based assessment. Subjective discomfort, personal impressions, or assumptions based on a customer's nationality, ethnicity, or profession are not legitimate bases for a SAR and could expose the professional to discrimination claims. The concern must be grounded in documented observable facts: a payment pattern, a structural anomaly, a documentation gap, a screening match.

Maintain strong documentation and clear case narratives. Every investigation must produce a written record that a third party — a regulator, a court, a supervisor — could read and understand without access to the professional's internal knowledge. The case narrative must explain what was observed, what it suggested, what was investigated, what was found, and what conclusion was reached. Vague notes are not documentation. A time-stamped, structured investigation record is.

Escalate through proper compliance channels. SAR decisions are not for individual agents to make. They must be escalated through the designated compliance officer, who is the person with the legal responsibility and the authority to make reporting decisions. An agent who identifies a concern must report it internally immediately. A compliance officer who receives an escalation must act on it systematically and within the applicable timeline.

Never tip off the customer. Once reasonable suspicion has been formed and internal escalation has begun, all communication with the customer must be managed with the tipping-off prohibition in mind. This includes not only direct statements about the investigation but indirect signals — unusual delays in processing, unexplained requests for additional documentation, or changes in the professional's behaviour that the customer might reasonably interpret as suspicion-related.

Apply the reasonable suspicion standard consistently. Consistency is both a legal requirement and a commercial necessity. A business that files SARs for some customers presenting equivalent risk indicators and not others — based on commercial factors, personal relationships, or differential treatment of different customer categories — is not applying the standard correctly and is creating documentary evidence of inconsistent compliance. The standard must be applied to every case on its own merits, regardless of the commercial value of the relationship.

What Changes Under the AMLR: July 2027 and SAR Obligations in Real Estate

The AMLR does not introduce the SAR obligation for real estate — it has existed under successive AML Directives since 2005. What the AMLR changes is the enforceability, consistency, and supervisory framework within which that obligation is assessed.

Direct applicability means that the SAR obligation applies identically in every EU member state from July 2027. The variation in national implementation that has historically allowed some markets to operate with lower de facto reporting standards is eliminated. Every professional in every member state is held to the same standard.

AMLA supervision means that SAR volumes, quality, and timeliness for real estate professionals in the highest-risk markets will be subject to direct EU-level scrutiny. AMLA's mandate includes ensuring the effectiveness of reporting as well as its occurrence. A business that files perfunctory, poorly documented SARs will not satisfy the standard any more than one that files none.

Expanded scope to letting agents at the €10,000/month threshold means that a large cohort of professionals who have never filed a SAR — and in many cases have never had a SAR filing process — must now build one. For letting agents, the triggers described in this article apply with full force: unusual tenant payment patterns, sudden high-value transfers, mule account payments of rent, and sanctions evasion through rental arrangements are all real risks in the high-value lettings market.

Strengthened FIU frameworks under the 6th AMLD mean that national FIUs are being resourced and structured to receive and process SARs from real estate professionals more effectively. The investment by authorities in the reporting infrastructure is accompanied by a corresponding expectation of higher reporting quality and volume from obliged entities.

Immosurance: The Infrastructure That Makes SAR Filing Possible

The compliance framework required to support correct SAR filing — systematic red flag detection, documented investigation, structured internal escalation, compliance officer accountability, and audit-ready record-keeping — cannot be managed through informal processes. It requires infrastructure specifically designed for the purpose.

Immosurance provides that infrastructure for every real estate business in Europe, regardless of size, market, or prior compliance experience.

Detection begins at onboarding and continues throughout the relationship. The platform's LexisNexis integration provides continuous sanctions and PEP screening with real-time alerts. The proprietary Real Estate Risk Module identifies transaction and customer patterns consistent with each of the seven SAR triggers described in this article. The ongoing monitoring architecture compares current transaction behaviour against the established customer profile, surfacing deviations for compliance officer review.

Investigation is supported through the client dossier architecture, which provides the compliance officer with the complete compliance history of every customer relationship at the point of alert review. The investigation log within each dossier allows the compliance officer to record observations, document enquiries made, capture responses received, and articulate the conclusion reached — creating the case narrative that both the good-faith protection and the AMLR's documentation obligation require.

Escalation is built into the platform's role-based workflow. When a monitoring alert is generated, it is routed to the compliance officer's dashboard. Escalation decisions — to file a SAR, to apply EDD, to continue monitoring, or to close the concern with documented rationale — are recorded within the dossier with timestamps and user identification. The compliance officer designation and backup designation are documented within the KYB module, ensuring that the structural accountability the AMLR requires is always in place.

Tipping-off protection is supported by the platform's access control architecture. SAR-related activities — the investigation log, the SAR consideration record, the compliance officer's escalation decisions — are restricted to the compliance officer role. Other platform users, including agents who have direct client contact, cannot access these records. The operational separation required to protect against inadvertent tip-off is built into the system structure.

Record-keeping for the AMLR's five-year retention obligation is managed automatically. Every alert, every investigation record, every SAR consideration decision, and every outcome is time-stamped, stored, and retained in accordance with the regulation's requirements. When AMLA or a national FIU requests records — for an ongoing investigation, a supervisory inspection, or a post-event review — the complete compliance history is available immediately, in a form that demonstrates both the quality of the compliance process and the good faith of the professionals who conducted it.

Conclusion: A Strong SAR Today Prevents Financial Crime Tomorrow

The source article ends with a sentence that deserves to be taken literally: a strong SAR today can help prevent financial crime tomorrow. This is not rhetoric. It is the mechanism by which the AML/CFT system functions.

Financial Intelligence Units analyse SAR data to identify criminal networks, map money laundering typologies, and build the intelligence picture that enables law enforcement to act. A single well-documented SAR from a real estate professional — describing an unusual transaction structure, a suspicious payment pattern, or an unexplained corporate ownership chain — can provide the link that connects an investigation targeting criminal proceeds worth millions.

The real estate professional who files that SAR does not need to know what happens next. They need only to have done their job: identified the suspicion, investigated it systematically, documented the findings, and reported through the correct channel. The AMLR creates the legal framework that requires them to do exactly that. Immosurance provides the operational platform that makes doing so practical, consistent, and defensible.

Every real estate business in Europe has, or will have, the circumstances that give rise to reasonable suspicion. The question is not whether it will happen. The question is whether the business will be equipped to handle it correctly when it does.